Featured

Table of Contents

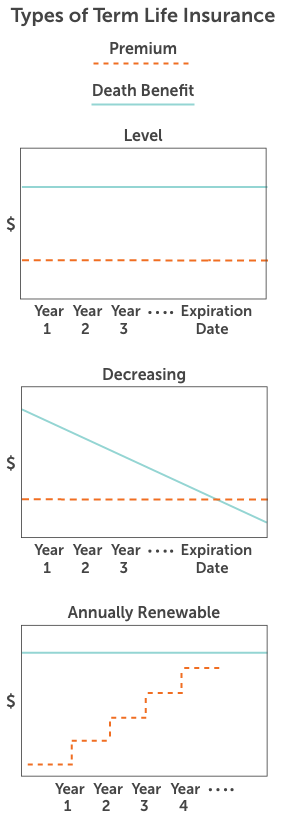

With degree term insurance policy, the expense of the insurance coverage will remain the very same (or potentially reduce if returns are paid) over the regard to your plan, normally 10 or 20 years. Unlike long-term life insurance, which never ends as lengthy as you pay costs, a level term life insurance coverage plan will certainly end at some time in the future, usually at the end of the period of your level term.

Because of this, many individuals utilize irreversible insurance policy as a secure financial planning device that can serve several requirements. You may have the ability to transform some, or all, of your term insurance policy during a collection period, typically the first 10 years of your plan, without requiring to re-qualify for coverage also if your health has actually transformed.

How much does Level Term Life Insurance Quotes cost?

As it does, you may intend to include in your insurance policy coverage in the future. When you first get insurance coverage, you may have little cost savings and a huge mortgage. Ultimately, your savings will certainly expand and your home mortgage will shrink. As this happens, you might intend to at some point reduce your fatality advantage or consider transforming your term insurance coverage to a long-term plan.

Long as you pay your costs, you can relax simple recognizing that your liked ones will certainly obtain a death advantage if you pass away during the term (Term life insurance with fixed premiums). Lots of term policies permit you the ability to convert to permanent insurance policy without needing to take one more health and wellness examination. This can allow you to make use of the extra advantages of a permanent plan

Lots of irreversible policies will include arrangements, which specify these tax demands. There are two basic classifications of permanent insurance, standard and interest-sensitive, each with a number of variants. On top of that, each category is typically readily available in either fixed-dollar or variable form. Standard entire life plans are based upon long-term estimates of expenditure, rate of interest and mortality.

If these estimates alter in later years, the firm will certainly readjust the costs appropriately but never above the optimum guaranteed premium stated in the policy. An economatic whole life plan attends to a basic quantity of participating whole life insurance coverage with an additional supplemental insurance coverage given through using rewards.

What is Compare Level Term Life Insurance?

Since the costs are paid over a shorter span of time, the costs settlements will certainly be higher than under the entire life strategy. Solitary premium whole life is minimal payment life where one large superior settlement is made. The policy is completely compensated and no additional premiums are called for.

Taxes will be incurred on the gain, nevertheless, when you give up the policy. You may borrow on the cash value of the policy, however remember that you may sustain a considerable tax obligation expense when you surrender, even if you have actually obtained out all the cash value.

The benefit is that improvements in rate of interest will certainly be shown quicker in rate of interest sensitive insurance than in conventional; the drawback, certainly, is that reduces in rates of interest will certainly likewise be felt quicker in interest delicate entire life. There are 4 standard rate of interest delicate whole life plans: The global life policy is actually greater than passion delicate as it is made to show the insurer's existing mortality and cost in addition to passion incomes instead of historic rates.

What is the best No Medical Exam Level Term Life Insurance option?

The business credit reports your costs to the cash value account. Occasionally the firm deducts from the money value account its expenses and the price of insurance policy defense, normally explained as the death deduction cost.

Existing assumptions are essential to passion sensitive items such as Universal Life. Universal life is also the most versatile of all the numerous kinds of policies.

The plan typically provides you a choice to choose a couple of sorts of survivor benefit. Under one choice your beneficiaries received just the face quantity of the plan, under the various other they receive both the face quantity and the cash money worth account. If you want the maximum amount of fatality benefit currently, the second alternative ought to be selected.

It is very important that these assumptions be reasonable since if they are not, you may have to pay even more to maintain the plan from lowering or lapsing. On the various other hand, if your experience is much better after that the assumptions, than you may be able in the future to miss a premium, to pay much less, or to have the strategy paid up at a very early day.

How do I choose the right Fixed Rate Term Life Insurance?

On the other hand, if you pay even more, and your presumptions are realistic, it is feasible to pay up the policy at an early day (Level term life insurance companies). If you give up a global life policy you might obtain less than the money worth account due to surrender charges which can be of two kinds

A back-end type policy would certainly be more suitable if you mean to keep protection, and the fee lowers with each year you continue the policy. Bear in mind that the rates of interest and expenditure and mortality charges payables originally are not assured for the life of the policy. This kind of policy gives you maximum adaptability, you will certainly require to actively manage the policy to preserve enough financing, especially because the insurance coverage business can raise death and expense costs.

You might be asked to make added premium repayments where insurance coverage can end since the rate of interest rate went down. Your beginning rates of interest is dealt with just for a year or sometimes 3 to five years. The guaranteed rate provided for in the plan is much reduced (e.g., 4%). One more function that is often stressed is the "no expense" car loan.

You must get a certificate of insurance defining the stipulations of the team policy and any type of insurance policy fee. Normally the maximum quantity of insurance coverage is $220,000 for a home loan and $55,000 for all other financial obligations. Credit history life insurance policy need not be bought from the company granting the finance

Why should I have Level Term Life Insurance?

If life insurance policy is called for by a creditor as a problem for making a car loan, you might be able to appoint an existing life insurance policy, if you have one. However, you may want to acquire team credit rating life insurance policy even with its greater price because of its comfort and its accessibility, usually without thorough proof of insurability.

However, home collections are not made and costs are sent by mail by you to the agent or to the firm. There are specific variables that tend to increase the prices of debit insurance even more than normal life insurance policy plans: Specific expenditures coincide no matter what the dimension of the policy, to make sure that smaller policies provided as debit insurance coverage will certainly have greater costs per $1,000 of insurance coverage than larger dimension regular insurance plan.

Given that very early lapses are pricey to a firm, the costs need to be passed on to all debit insurance policy holders. Since debit insurance is made to include home collections, higher compensations and costs are paid on debit insurance than on normal insurance coverage. In a lot of cases these greater expenses are handed down to the policyholder.

Where a company has various costs for debit and normal insurance coverage it might be possible for you to acquire a bigger amount of routine insurance policy than debit at no extra price. For that reason, if you are assuming of debit insurance coverage, you must definitely check out regular life insurance as a cost-saving alternative.

What is included in Guaranteed Level Term Life Insurance coverage?

This strategy is made for those that can not initially afford the regular whole life premium however that desire the higher costs protection and feel they will become able to pay the greater costs. 20-year level term life insurance. The household plan is a mix plan that supplies insurance coverage security under one contract to all participants of your instant family members hubby, spouse and children

Joint Life and Survivor Insurance gives protection for two or even more individuals with the death benefit payable at the death of the last of the insureds. Premiums are substantially lower under joint life and survivor insurance than for plans that insure just one person, given that the chance of needing to pay a fatality insurance claim is reduced.

{kind=link}

Latest Posts

Whole Life Insurance Instant Quote

Best Final Expense Insurance Companies

Instant Online Quote For Life Insurance